Is climate change the new slavery?

April 17, 2014

National Security and Foreign Policy Priorities in the FY 2015 International …

April 17, 2014

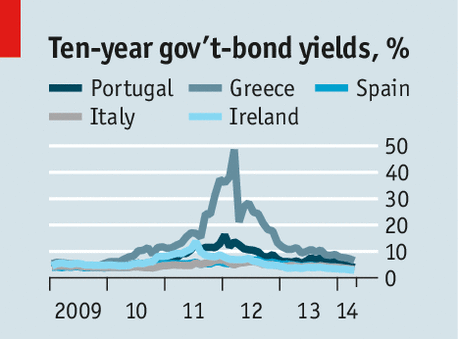

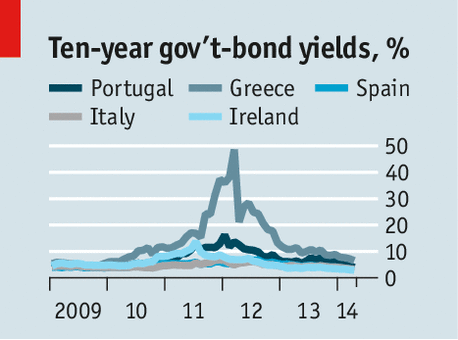

INVESTORS have developed a remarkable enthusiasm for the European debt they once shunned. On April 10th, only two years after Greece imposed the biggest debt-restructuring in history on its private creditors, it raised €3 billion ($4.1 billion) in five-year bonds at a yield of less than 5%; the issue was seven times oversubscribed. On April 15th yields on ten-year Italian-government bonds fell to 3.11%, the lowest on record. From Portugal to Ireland, investors are piling into the bonds of the euro zone’s peripheral economies, pushing nominal yields down to levels not seen since the single currency began.

It is tempting to say that this is proof that the euro crisis is over: that years of tough reform are paying off, and that lower bond yields should soon lead to greater investment and faster growth. Tempting, but largely wrong. The outlook is far less rosy than the plunge in bond yields suggests. First, there is the cruel arithmetic of deflation. With prices falling in several of the peripheral economies, the real burden of their debts is rising. Second, much of the fall in bond yields reflects investors’ hopes that the European Central Bank (ECB) will start printing money, hopes that are likely to be dashed.

Insatiable

A year ago Spain’s ten-year bonds yielded 4.7% and its inflation rate was 1.5%. Today ten-year bonds yield 3.1%, but inflation has fallen below zero. On this crude measure, the real yield on these government bonds—that is, after adjusting for inflation—has barely budged. On a fancier measure, using ten-year inflation expectations, real yields on the periphery’s sovereign bonds have fallen more, but are still much higher than anywhere else in the rich world. That is why investors are piling in. But it is also why the debt burden is a problem.

Hoping against history

The burden of a country’s debts depends on how much it owes and the gap between its growth rate and the real interest rate it must pay. On each count, Europe’s peripheral governments fare poorly. Most have debts above 100% of GDP. Structural reforms, from freeing labour markets to deregulating cosseted industries, have not been radical enough to transform their growth prospects (see article). So the odds are that output will stay weak, deflation will persist and debt will rise further.

The way to avoid this is strong action from the ECB to banish deflation. That is exactly what many investors today are betting on. Thanks to a string of hints from ECB officials that they are considering “unconventional measures” to stop inflation falling further, there is a growing expectation that the ECB is on the brink of cranking up the printing presses.

The reality will probably be much less dramatic. Europe’s central bankers are willing to talk about bold measures, in the hope that talk alone persuades the markets. But there is no evidence of a commitment to act decisively. Germany’s influential Bundesbank is not convinced that low inflation is yet a problem. Even those central bankers who worry about falling prices see endless practical problems in designing measures to combat them. If the ECB acts it will probably be in small, careful steps, starting perhaps with the introduction of a negative rate on bank deposits.

Unfortunately, history suggests that incremental efforts to fight deflation do not work. Take Japan. For two decades the economy was stuck in a trap of economic stagnation, falling prices and rising debt. In the early 2000s the Bank of Japan’s timid efforts at battling deflation with money-printing failed. Only since 2013 has the ambitious stimulus of Abenomics begun to succeed. The ECB is much more like the Bank of Japan in 2000 than that of 2014. Until that changes, investors in Europe’s periphery should expect more deflation and rising debt. Nominal yields may shrink further, but the problems are not getting any smaller.

{kind=link}