Patriots president talks bullying, sports at ADL event

May 29, 2014EU Commission Rejects Plea to Block Stem Cell Research Funding

May 29, 2014

Piketty: Ed Alcock; Roubini: Pete Marovich/Bloomberg; Bieber: Tony Barson/Filmmagic/Getty Images; Marx: GL Archive/Alamy

Piketty: Ed Alcock; Roubini: Pete Marovich/Bloomberg; Bieber: Tony Barson/Filmmagic/Getty Images; Marx: GL Archive/Alamy

A specter is haunting Europe and the U.S.—the specter of plutocracy. In Britain, Deputy Prime Minister Nick Clegg has suggested the moment has arrived to consider a wealth tax. In France, which already has one, plans to ease its bite were recently canceled. Even in the more timid precincts of Washington, you cannot swing a V for Vendetta mask without hitting a think tank panel on inequality. Everyone, it seems, is worried we are shortly headed for a world in which a handful of rich people will own everything, and the rest are forced to rent their air and water from Mark Zuckerberg.

Small wonder, then, that French economist Thomas Piketty’s Capital in the Twenty-First Century has ignited an ideological fervor reminiscent of a Paris mob at the gates of the Bastille. The title seems to be a puckish homage to Karl Marx’s Capital. Although Piketty disdains Marx’s unsystematic thinking, they share a core concern about wealth run amok or rather too much concentrated in one place. Piketty speaks for a lot of people when he voices a dark half-prophecy that the forces of capital accumulation will leave us with a society radically less equal, less mobile, perhaps even less democratic. As he puts it, “The past devours the future.”

Booksellers have been unable to keep Capital on their shelves. (The physical version is vastly more popular than the Kindle edition; people apparently prefer to haul around the 700-page tome, or maybe leave it on the coffee table where guests can see it.) Its publisher, Harvard University Press, is rushing out another printing of the hardcover. This runaway success may not seem too surprising in an era when President Obama has called inequality “the defining challenge of our time.” However timely the argument, the book itself is not what one thinks of as popular reading. “When the book came out,” says economics professor Brad DeLong, of the University of California at Berkeley, “I thought it had an audience of three people in Berkeley”—himself, economic historian Barry Eichengreen, and Christina Romer, former head of the president’s Council of Economic Advisers.

Tyler Cowen, an economics professor at George Mason University, writes in Foreign Affairs that “although the book’s prose (translated from the original French) might not qualify as scintillating, any educated person will be able to understand it—which sets the book apart from the vast majority of works by high-level economic theorists.” There’s surprisingly little math or jargon and a delightful number of literary references to illustrate the historical evolution of capital in rich societies. Which by no means erases the fact that Capital in the Twenty-First Century is still a book by an economist for people who find it comfortable, even enjoyable, to have a little light algebra in their beach reading. How did this book work its way to the top of Amazon.com’s (AMZN) ranks, right up there with The Conscious Parent and Frozen Little Golden Book?

Part of the answer is controversy. Liberals love its affirmation of their sense that the rich have never been richer, while conservatives worry it is an attempt to steal a base in the ongoing battle to tax private wealth. Capital in the Twenty-First Century is a perfect stand-in for collective anxiety about the fate of the middle class, from Occupy Wall Street’s concern that the 1 Percent are leaving the rest of us to an increasingly impoverished future, to the growing worry on the right that inequality springs from and is creating a vicious cycle of economic instability and cultural breakdown among the two-thirds of the American population who lack a college diploma. The book doesn’t speak to our current situation nearly as much as many buyers probably think. But the conversation it has provoked very much does.

Photograph by Ed AlcockThomas PikettyPiketty, 43, has been famous among economists for some time. The child of working-class parents who took part in the French student uprisings of 1968, he completed his Ph.D. at France’s L’Ecole des Hautes Etudes en Sciences Sociales at an age when most American students are still wrapping up their undergraduate years. He moved to Boston to teach economics at the Massachusetts Institute of Technology and quickly concluded there was something missing from American economics. In the introduction to Capital in the Twenty-First Century, he writes, “My thesis consisted of several relatively abstract mathematical theorems. Yet the profession liked my work. I quickly realized that there had been no significant effort to collect historical data on the dynamics of inequality since [Simon] Kuznets, yet the profession continued to churn out purely theoretical results without even knowing what facts needed to be explained. And it expected me to do the same.” He returned to France and “set out to collect the missing data.”

Photograph by Ed AlcockThomas PikettyPiketty, 43, has been famous among economists for some time. The child of working-class parents who took part in the French student uprisings of 1968, he completed his Ph.D. at France’s L’Ecole des Hautes Etudes en Sciences Sociales at an age when most American students are still wrapping up their undergraduate years. He moved to Boston to teach economics at the Massachusetts Institute of Technology and quickly concluded there was something missing from American economics. In the introduction to Capital in the Twenty-First Century, he writes, “My thesis consisted of several relatively abstract mathematical theorems. Yet the profession liked my work. I quickly realized that there had been no significant effort to collect historical data on the dynamics of inequality since [Simon] Kuznets, yet the profession continued to churn out purely theoretical results without even knowing what facts needed to be explained. And it expected me to do the same.” He returned to France and “set out to collect the missing data.”

In 2001, Piketty published a book on the evolution of inequality in France, using public records such as tax collections. By 2003 he was ranging beyond his home country, publishing an influential paper titled “Income Inequality in the United States, 1913–1998” with Berkeley’s Emmanuel Saez. Piketty and Saez’s data show that inequality peaked in 1929, followed by a long decline during which economists such as Kuznets optimistically theorized that technological progress was reducing the gap between the top and the bottom. Then, in the 1980s, inequality began to widen again, reaching levels not seen since the early 20th century.

Over the past decade, Piketty, along with Saez and others, has deepened and expanded his work on income inequality, which eventually blossomed into the World Top Incomes Database. This work has been especially popular with the left—Piketty’s become one of its standard bearers in France. He took a break from his academic career to advise Socialist Party candidate Ségolène Royale when she ran for the presidency, and though he has not been an official adviser to the current Socialist president, François Hollande, he did join 41 other economists in signing a public letter of support. (This is not as startling as it may sound to American ears; the Socialist Party is France’s major left-wing political faction, akin to Labour in Britain and the Democrats in the U.S.)

Piketty’s book is an expansion of his earlier work but also a significant departure: For the first time he is attacking the problem of wealth inequality, as well as income inequality. People frequently speak as if the two are interchangeable. They are in fact quite distinct—one does not imply the other—and part of what makes Capital in the Twenty-First Century so important is that it provides a comprehensive account of the coevolution of income and capital.

The first thing to understand about Capital is that it is not really one book. There’s a data book, an analysis book, a book of projections about the future, and a book of policy recommendations based on those projections. All four are packaged within its 700 pages and frequently interleaved. Each has different strengths and weaknesses, a different style of argument, and a different audience—and when you see commentators yelling at each other about the contents, it’s probably because they’re talking about different books.

The first is an extensive elaboration of the kind of exacting data collection Piketty has been publishing with Saez for more than a decade. Here are enormous quantities of information distilled from tax rolls, inheritance records, and various other public data sources, laid out in charts that should be readily accessible to the layest of lay readers. Not all of the information in these sections is novel or startling. Having it together in one place, however, is valuable, and even most of the book’s fiercest critics respect this achievement. Former Treasury Secretary Larry Summers, who faults it for misunderstanding some concepts, calls it “deeply grounded in painstaking empirical research.”

Over the last few weeks, however, Piketty has taken some knocks. Four French economists published an article arguing that his results on rising wealth are largely driven by the Europe-U.S. housing bubble, which has pushed up home prices but not necessarily rents. This could seriously undercut Piketty’s thesis in one of two ways: Home prices could fall back toward previous levels as central banks begin raising interest rates, or they could keep rising much faster than rents—in which case, the return on large amounts of our capital stock would fall.

On May 23, Chris Giles, economics editor of the Financial Times, alleged serious errors in Piketty’s work. Giles went through the data, which Piketty makes available to all on the Web. He claimed to have found flaws ranging from minor transcription errors to an inexplicable divergence between Piketty’s data on British wealth inequality and the data sets the professor cites. The British data divergence is troubling, because it appears to show wealth inequality basically flat, rather than increasing, which means Piketty’s data for increasing wealth concentration in Europe rest heavily on France and Sweden.

In an e-mail to Bloomberg News, Piketty rejects these arguments, saying “there’s no mistake or error” in his work. This might be a bit strong—what superman has published 700 pages without so much as a misplaced decimal point? And even many of his critics seem to agree the supposed errors aren’t fatal. Scott Winship of the Manhattan Institute for Policy Research, who has spent a lot of time with Piketty’s spreadsheets on income inequality, doesn’t think the Financial Times story will significantly damage Piketty’s work. Even before these charges broke, Harvard University economics professor Kenneth Rogoff told me, “The broad theme that income and wealth inequality have gone up has been found by other people in other ways, and it’s true.”

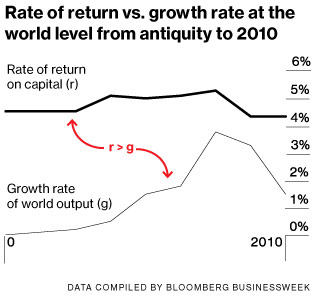

When Capital in the Twenty-First Century turns to analysis, Piketty deftly works in Honoré de Balzac and Jane Austen. But the heart of this section is more algebraic than literary: r g has become a somewhat unlikely catchphrase among many left-leaning commentators. In English, what this means is that the rate of return on capital, r, is higher than the growth rate of the economy as a whole, g. In even plainer English, this means income from investments will grow faster than wages.

Piketty dubs this the central contradiction of capitalism and spends much of Capital teasing out its implications. He concludes that, if left unchecked, capital tends to grow faster than the economy; so over time, the ratio of wealth to income soars. He details a dire possible future that looks a lot like the past—which is to say, a world in which inheritance trumps almost every other possible way of making money. There’s a reason that characters in Victorian novels spend so much time scheming to marry heiresses, murdering inconvenient older brothers, and ingratiating themselves with rich uncles. It’s more profitable than working.

The idea that r is greater than g itself is not so disputed. “Of course r is greater than g,” says Rogoff. Winship says it’s “basically noncontroversial, because you have to have some compensation for risk.” People who save and invest their money are choosing to trade away today’s income in exchange for income tomorrow. Investments have to pay a premium to get people to park their money—and since the future is uncertain, that premium has to be pretty large.

What superman has published 700 pages without so much as a misplaced decimal point?

As Piketty lays out the implications of r g, however, the critics begin to get restive. There are a lot of petty complaints—some of the literary references don’t make quite the point he thinks, and he’s a bit slippery when moving between different categories of capital. The biggest complaint is that his results depend heavily on his assumptions—and his assumptions are not necessarily good. “Even if one grants r g, capital may grow more rapidly than output, less rapidly, or at the same pace,” says a critique by Stefan Homburg of Germany’s Institute of Public Finance. In other words, even if the return on capital is higher than the growth rate of the economy, that doesn’t mean capital will accumulate and concentrate itself indefinitely; the capitalists might spend it, give it away, or divide it among heirs faster than it accumulates. Even Piketty acknowledges that capital will not accumulate forever, as Marx predicted. Eventually he thinks capital will stabilize, so it’s no longer growing faster than national income—albeit at a much higher level than currently.

Whether he’s right depends on a number of things. For example, as the stock of capital gets larger, the return on each additional dollar invested into capital is likely to fall. If you’re the first person to open a fast-food restaurant in your town, the return on your investment is probably pretty high. If you’re the 80th, you should have more modest expectations. Piketty assumes that the return on capital will stay high enough to keep capital incomes rising for a good long while, even as growth in the rest of the economy slows because of a variety of technological and demographic factors.

Why the assumption? For one thing, his data show that return on capital was high before the Industrial Revolution, when rates of growth were very low. There’s a problem with this: Piketty doesn’t really have good data for the period before the Industrial Revolution. So he just infers a rate based on what information we have about land rents and interest rates. While that’s perfectly fair, it gives credence to the critique that he’s bolstering an assumption about the future with yet another assumption about the past.

Much of the debate about the work has taken place at a level few of his readers are likely to be willing—or able—to follow. Take, for example, the back and forth over the elasticity of substitution between capital and labor. In economics jargon, Piketty theorizes that the elasticity of substitution is greater than one. He’s saying it’s roughly as easy to increase your production with an investment, such as buying another machine, as it is to increase it by hiring another worker. This is controversial: As Summers recently wrote in Democracy, “I know of no study suggesting that measuring output in net terms, the elasticity of substitution is greater than 1, and I know of quite a few suggesting the contrary.”

If, as Summers and others argue, labor and capital aren’t very good substitutes—meaning additional dollars invested require new workers to make the investment profitable—then over time, as capital grows faster than the labor force, the return on new investment will fall pretty sharply, either because you can’t get workers to operate your machines or you have to pay them higher wages to get them to work for you. On the other hand, if it’s relatively easy to substitute capital for labor—imagine staffing your fast-food restaurants with hamburger-cooking machines and order-taking computers that never take a break and don’t demand raises or health insurance—then additional investments may be made at a high rate of return. Berkeley’s DeLong explains Piketty’s future in a single word: “Robots!”

OK, but how many of them will we buy? How fast capital accumulates also depends on the behavior of the capitalists. Do they take their extra income and reinvest it in more income-producing capital? Or do they invest it in extravagant vacations, designer clothes, and rapidly depreciating yachts? Piketty assumes that the savings rate will stay steady; this is not necessarily the most obvious assumption. Even investments in robots are not infinitely productive, which you can see by looking at your own house. The dishwasher saves you hours of work every week; your washer-dryer saves a whole day, which is what it took your great-grandmother to wash everyone’s clothes. Buying a Roomba might save you an hour vacuuming every Saturday morning, and a machine to clean windows saves time only on a scale of months or years. So it is with industrial robots: Over time, each additional machine is apt to create less and less value relative to its cost. So maybe you put the money into a nicer vacation instead or give it away.

This might not hold for the giant fortunes that Piketty worries are accumulating. Even if Bill Gates decided to devote every waking hour to sybaritic enjoyment, his money would quite probably pile up faster than he could spend it. On the other hand, Gates and Warren Buffett have committed to give a huge portion of their fortunes to charity. Spreading inheritances across large families will dissipate large fortunes, although less quickly as life spans lengthen. In countries with low birthrates, Piketty’s capital accumulation could be dramatically sped up by demographics, as one child inherits from four grandparents.

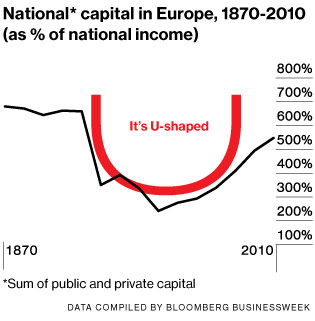

The taxes, dislocation, and sheer physical destruction involved in fighting large-scale wars appear to be devastating to wealth. Piketty’s analysis shows a U-shaped curve for European capital in the 20th century: It starts at a peak on the eve of World War I, then quickly declines, bottoming out from 1950 to 1970 before beginning to rise sharply again.

Piketty’s work suggests that this era was an historical anomaly, and he predicts that capital will dominate the future as it did before the wars. But predicting the future can be hard work. Imagine an ancestral Thomas Piketty sitting down in 1913 to write Capital in the Twentieth Century. Such a book would probably have shown a continuation of long-term trends, with a tiny European elite deriving most of their outsize income from investments or land. He would probably predict that capital income, which had recently been rising in Britain and France after a 30-year decline, would continue to soar. In other words, his major prediction would have likely been totally wrong.

By extension, any policy changes he suggested would also be wrong. This section of the book, and especially Piketty’s proposal of a global tax on wealth to prevent the accumulation of massive fortunes, is almost universally viewed as the weakest. “I suspect he doesn’t take that seriously himself,” Rogoff says of the wealth tax. “First of all, it’s next to impossible to implement. The EU can’t even implement one.” Another question is what he plans to do with the money thus raised. Inequality between countries remains much larger than inequality within countries, and it is hard to imagine certain transfers. “Does he mean to have a wealth tax on the French middle class and send the money to Africa?” asks Rogoff. It’s safe to assume this is not what most of the book’s purchasers have in mind.

DeLong, who’s been one of the book’s staunchest defenders, agrees this is the weakest section of Piketty’s opus. “There are many things we could do,” he says. Trying to corral a couple of hundred nations into a massive cooperative tax scheme is only one, and probably not the most practical. Wealth taxes were adopted by a lot of countries in the 20th century; most abandoned them, because the rich people kept moving abroad and taking their capital with them. That’s why Piketty has proposed making his wealth tax global. As Rogoff points out, however, this substitutes one political economy problem for the even larger difficulty of getting every last nation on the earth to agree to impose it.

Even if we assume Piketty’s prediction is correct, that economic forces favoring capital will cause it to accumulate and concentrate in the hands of a hereditary superelite, and even if we assume his remedies would work, that leaves one big question to debate: Is this really the most important issue facing the world, “the defining challenge of our time”?

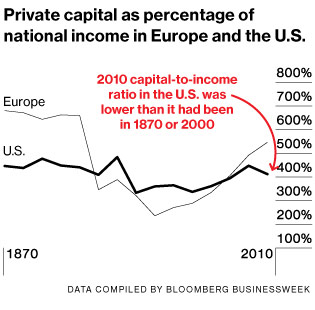

The most remarkable thing about Piketty’s book is that it owes its popularity to U.S. audiences. When Capital in the Twenty-First Century was published in France last year, it sat quietly on the shelves. Only after it became an American bestseller did French consumers start snapping it up. This might seem only natural; the U.S., after all, is where income inequality is extreme. But Piketty’s book is primarily about wealth inequality. Income can create wealth, though if that happens, it will be far in the future. And right now, as the book shows, wealth inequality is far less pronounced in the U.S. than in Europe. The dramatic U curve in European wealth is practically flat in America, where the capital-to-income ratio in 2010 was lower than it had been in 1870—or 2000.

Instead of the interest-collecting gentry of Jane Austen novels, we have Horatio Alger’s entrepreneurs on the make—an elite of doctors, lawyers, CEOs, financiers, professional athletes, and movie stars who mostly did not inherit their wealth. Yet Capital in the Twenty-First Century is not a hit because Americans think it tells them something important about what our great-grandchildren will be doing in 2070. They think it tells them something important about what’s happening right now—and in the U.S., not in France.

Illustration by Neal Fox

Illustration by Neal Fox

They’re not wrong that something is happening in the U.S. While people do hate the idea of a landed gentry with huge trust funds—think of the 1 Percent owning more than a third of all wealth—that’s not actually what’s driving the troubling trends. A society that used to offer broad security, stability, and opportunity to the top 75 percent of households is now increasingly divided into an educated elite and a low-skilled workforce for whom work is uncertain and not very well paying. This doesn’t just make it harder to sustain the iconic single-family home on a nice lot; it makes it harder to form stable families and communities. Among people without a college diploma, life looks more and more like it did for the welfare-dependent underclass in the 1980s: exploding levels of single parenthood with multiple partners and low levels of participation in civic groups such as churches and bowling leagues. People living in this environment are more financially and emotionally vulnerable; children are more likely to drop out of school and the labor force.

Among the educated, marriage is great, healthier than ever. But looking at the chaos at the bottom, and forced to compete with the superrich for college slots and houses in good school districts, many, even among the well educated, are terrified they won’t be able to assure their children a place in the middle class—especially since their own jobs, while more secure than the loading dock work at Walmart (WMT), are more vulnerable to layoffs than they used to be. All this is made scarier still by the rising cost of health care and college tuition.

Of course, this is partially a story about capital: Robots actually have replaced a lot of jobs and will replace more in the future. From computers that take your order at McDonald’s (MCD) to search software that can replace dozens of lawyers and paralegals in the lawsuit discovery process, capital is becoming a better substitute for many forms of labor—and the people who did that labor are having trouble finding replacement jobs that will pay them as well as their old ones did.

This is also a story about globalization. The rise of China has added a billion people to the global workforce, most of them willing to work for much less than an American autoworker. Immigration has brought low-wage competition for construction workers and landscapers. The Internet and the emergence of robust global markets have increased the returns available to people at the very top. Everything from consumer electronics to movies are sold in a single world market, which means the winners get paid more than ever. The losers can no longer survive by finding a smaller pond, as the global marketplace has blown away local niches.

While global markets make capital more valuable, they also destroy a lot of capital; just ask the people who owned the factories now rusting along half the highways in the Midwest. Trade and immigration are massive transfers not necessarily from labor to capital, but from labor to labor: rich world workers to poor ones. As a result, global inequality has fallen, even as inequality within countries has risen.

“If you took the whole world as a country, you’d be pretty excited about what has happened over the last 30 years,” says Rogoff. Of course, if you’re a steelworker in Ohio, that’s cold comfort.

Piketty’s proposal for higher taxes, including a wealth tax, might stop wealth from accumulating in quite such dramatic piles. What it can’t do is roll back the automation and globalization processes that have so many people so terrified; at best, it would slow the pace. We could use the proceeds of a wealth tax to ease some of the pain, but even in countries with a generous social safety net, long-term unemployment is miserable.

Judging from the reviews and the reaction and commentary, most readers are probably not looking to tease out these sorts of complications. They are interested in the book’s broad sweep, in Piketty’s evidence that they are right to feel something is wrong. Many are probably less interested in the book than what people are saying about it. That’s one legacy the book’s author can count on. Whatever the public verdict on his data, whatever future economists say about his theory and predictions, Piketty has touched off the most vigorous public conversation about inequality since Occupy Wall Street—only this time it’s a conversation about data and economics, rather than the wealth of certain bankers and the propriety of camping in the streets. That’s a lot of progress to come from one man.